Plenary Speech by IMF First Managing Deputy Director Gita Gopinath at twentieth World Congress of the Worldwide Financial Affiliation Colombia

Introduction

Good morning. It’s an honor to talk on the 20th World Congress of the Worldwide Financial Affiliation.

The overarching query of this congress is “Are we at a turning level?”

I imagine we’re. In truth, I’ll take this congress’ query a step additional and ask: are we getting ready to Chilly Struggle II? The historian Niall Ferguson argues that we already are. In that case, what would that imply for the worldwide financial system? And the way can we protect the positive factors from financial openness inside a extra fragmented world?

To reply these questions, I’ll first briefly hint the historical past of cross-border commerce relations in the course of the twentieth century. I’ll then study the parallels and variations between the Chilly Struggle and right this moment. I’ll describe the indicators of fragmentation that we see in commerce and funding knowledge to date and talk about the potential financial prices ought to the fault strains deepen. Lastly, I’ll provide three ideas for shielding financial cooperation in a extra fragmented world.

Pandemic, conflict, and rising tensions between the 2 largest economies of the world—the US and China—have undoubtedly modified the playbook for international financial relations. The US requires “friend-shoring,” the EU for “de-risking,” and China for “self-reliance.” Nationwide safety considerations are shaping financial coverage worldwide.

In the meantime, the worldwide rules-based system was not constructed to resolve nationwide security-based commerce conflicts. So, we now have international locations strategically competing with amorphous guidelines and with out an efficient referee.

There are advantages for international locations of this playbook as they try to de-risk their provide chains and strengthen nationwide safety. However, if not correctly managed, the prices may simply overwhelm these advantages, and probably reverse almost three a long time of peace, integration, and progress that helped carry billions out of poverty.

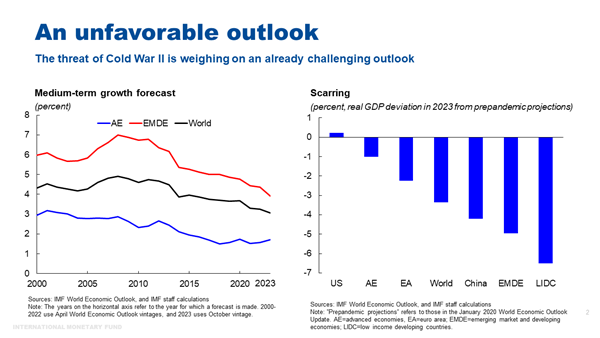

With the weakest international progress prospects in a long time—and with disproportionate scarring from the pandemic and conflict slowing revenue convergence between wealthy and poor nations—we are able to little afford one other Chilly Struggle.

Some historic perspective

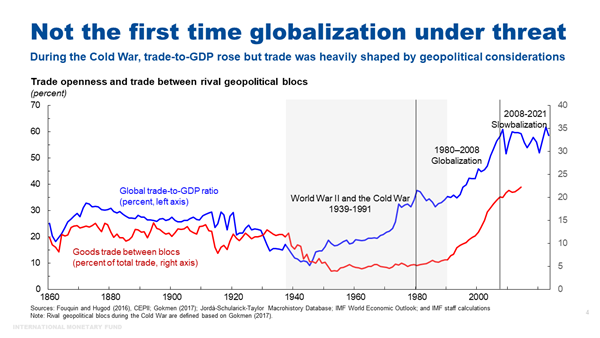

Let’s begin by trying on the historical past. This isn’t the primary time that globalization has come below risk and geopolitical issues have fragmented international commerce and capital flows. [1]

There was an explosion of worldwide commerce in the course of the “lengthy” 19th century, a 125-year interval starting with the French Revolution in 1789. However WWI introduced that golden period of globalization to an abrupt finish with world commerce collapsing as a share of revenue. The protracted financial hardship that adopted the conflict paved the way in which for the rise of nationalist and authoritarian leaders that later plunged the world into WWII. After WWII, a fragmented bipolar world emerged with two superpowers—the US and USSR—divided by ideology, and political and financial buildings. Poised precariously between them was a set of non-aligned international locations.

This “Chilly Struggle” interval, between late Forties and late Eighties, was not a interval of de-globalization because it was marked by rising international commerce to GDP pushed by the post-war restoration and the commerce liberalization insurance policies adopted by many international locations within the Western bloc. Nevertheless, it was a interval of fragmentation as commerce and funding flows have been closely formed by geopolitical issues. Commerce between opposing blocs collapsed from round 10-15 % to lower than 5 % of world commerce in the course of the Chilly Struggle.

With the top of the Chilly Struggle, commerce between beforehand rival blocs expanded quickly, reaching nearly 1 / 4 of world commerce within the following decade. The top of the Chilly Struggle additionally coincided with the hyper-globalization interval of the Nineteen Nineties and 2000s: technological improvements, unilateral and multilateral commerce liberalization, and geopolitical and institutional modifications all coalesced to carry financial integration to ranges not seen earlier than.

Since 2008, nonetheless, the tempo of globalization has stagnated—the so-called slowbalization—with commerce to GDP stabilizing because the forces that helped spur hyper-globalization naturally waned. [2]

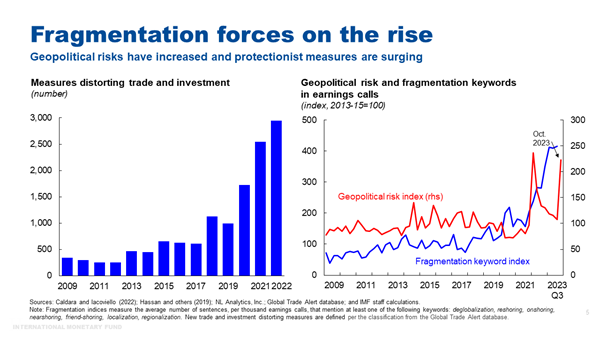

That brings us to the current day. Over the previous 5 years, threats to the free move of capital and items have intensified as geopolitical dangers have grown. Some measures, together with tariffs or export restrictions, immediately goal commerce and funding. Different behind-the-border measures not directly have an effect on commerce flows, akin to fiscal and monetary help to particular home sectors and native content material necessities.

Round 3,000 commerce proscribing measures have been imposed final yr—almost 3 occasions the quantity imposed in 2019.

Multinational companies, of their earnings’ calls, are more and more discussing points akin to re-shoring, near-shoring, friend-shoring, and deglobalization.

Chilly Struggle II?

So are we initially of Chilly Struggle II? The important thing driving drive is comparable—that’s the ideological and financial rivalry between two superpowers. Within the Chilly Struggle it was US and Soviet Union, now it’s US and China.[3] However the stage on which these forces are unleashed is essentially completely different alongside a number of dimensions.

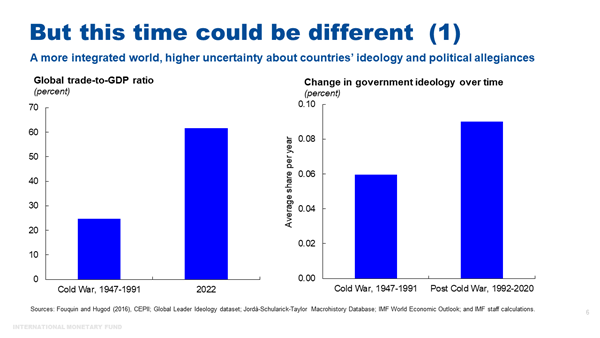

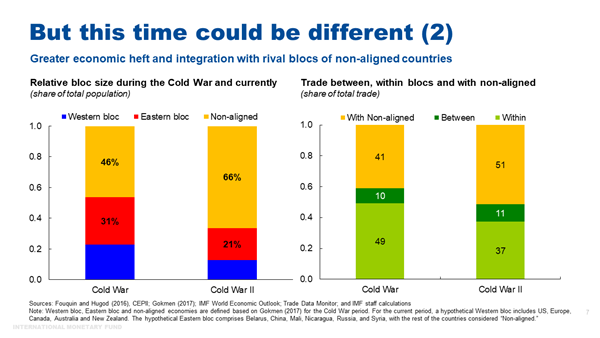

To begin, the diploma of financial interdependence between international locations now’s larger, as economies have change into rather more built-in into the worldwide market and thru advanced international worth chains. World commerce to GDP is now 60 % in comparison with 24 % in the course of the Chilly Struggle. This can probably increase the prices of fragmentation.

There’s additionally higher uncertainty on the bloc with which international locations could select to affiliate. Inside-country swings within the ideology of the political management have elevated in comparison with the Chilly Struggle period and make it troublesome to pin down allegiances. This uncertainty can additional increase prices.

However, the possibly non-aligned international locations now have higher financial heft when it comes to GDP, commerce, and inhabitants. [4] For the present interval, the evaluation considers two hypothetical blocs primarily based on international locations’ voting patterns within the UN and embrace predominantly the US and Europe within the Western bloc and China and Russia within the Japanese bloc, with the remainder of the international locations thought of “non-aligned.” In 1950, the Western and Japanese blocs collectively accounted for roughly 85 % of world GDP. The 2 blocs that we hypothetically have right this moment account for roughly 70 % of GDP and solely one-third of the world’s inhabitants. They usually should compete with non-aligned rising gamers.

Given their elevated financial integration—in 2022 greater than half of world commerce concerned a non-aligned nation—they will function “connectors” between rivals. They’ll profit immediately from commerce and funding diversion in a fractured international financial system and cushion the destructive impact of fragmentation on commerce, subsequently decreasing its prices.

Rising fault strains: The details about fragmentation

Let’s subsequent study the details about fragmentation. As you will note, there are indicators of rising fault strains.

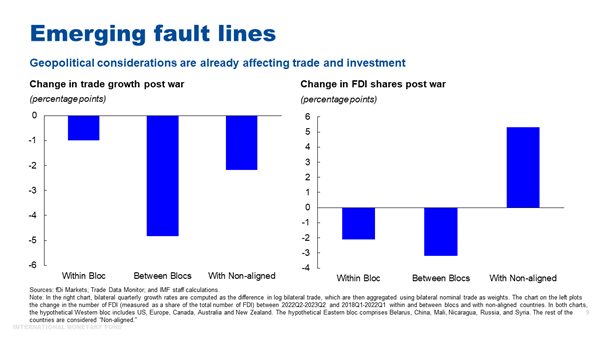

Just like the interval of the Chilly Struggle, we don’t see significant deglobalization, because the share of world commerce in world GDP stays comparatively steady. However we’re starting to see indicators of fragmentation with significant shifts in underlying bilateral buying and selling relations.

Whereas the expansion of commerce has slowed in every single place after the conflict in Ukraine, progress between blocs that aren’t politically aligned has slowed extra. Particularly, commerce progress inside blocs has decreased to 1.7 % from 2.2 % pre-war. Commerce between blocs has declined from 3 % pre-war to round -1.9 %. On internet, this generates 3.8 proportion level sooner progress in commerce inside blocs versus between blocs.

Importantly, this sample will not be restricted to simply commerce in strategic sectors—that are almost certainly to be focused by policymakers and probably helps international locations de-risk. It additionally seems in commerce of non-strategic merchandise.

There are additionally clear indicators that international international direct funding (FDI) is segmenting alongside geopolitical strains. [5] Introduced FDI initiatives between blocs declined greater than these inside blocs after the onset of the conflict in Ukraine, whereas FDI to non-aligned international locations sharply elevated. In truth, nearly 40 % of introduced FDI initiatives have been in these economies in 2023q3.

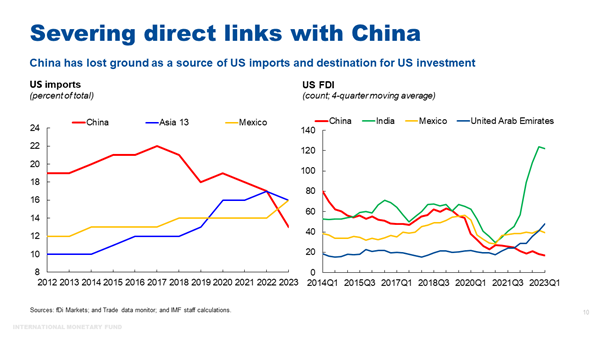

This occurred alongside the resurgence of commerce tensions between the US and China, between whom direct hyperlinks are being severed.

China is not the biggest buying and selling associate to the US, and its share of US imports has fallen by nearly 10 proportion factors in 5 years: from 22 % in 2018 to 13 % within the first half of 2023. The commerce restrictions imposed for the reason that onset of the US-China commerce conflict in 2018 have successfully curbed Chinese language imports of tariffed merchandise. [6]

China can also be not a outstanding vacation spot for outward US FDI, shedding rank to rising markets akin to India, Mexico, and UAE within the variety of introduced FDI initiatives.

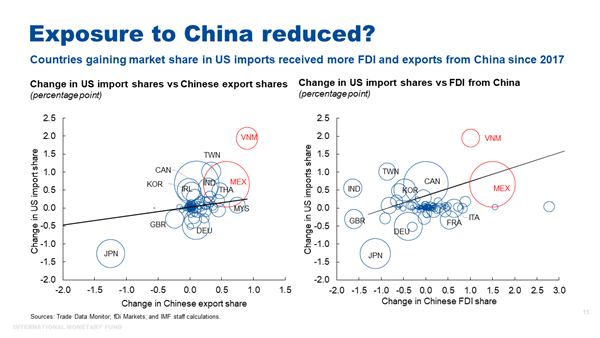

However there’s suggestive proof that direct hyperlinks between US and China are merely being changed by oblique hyperlinks. International locations which have gained essentially the most in US import shares—akin to Mexico and Vietnam—have additionally gained extra in China’s export shares. [7] The identical international locations are additionally bigger recipients of Chinese language FDI.

There’s rising anecdotal proof of a set of “connector” international locations which might be uniquely positioned to learn from the US technique of “de-risking” from China. This is because of components akin to their location, pure endowments, and free commerce agreements with either side.

For instance, massive electronics producers have accelerated relocating manufacturing from China to Vietnam given US tariffs on Chinese language items. Nevertheless, Vietnam sources most inputs from China, whereas most exports go to the US.

In the meantime, Mexico eclipsed China as the most important exporter of products to the US in 2023. However many producers opening vegetation in Mexico are Chinese language corporations, concentrating on the US market. In line with the Mexican Affiliation of personal industrial parks, one in 5 new companies within the subsequent two years can be Chinese language.

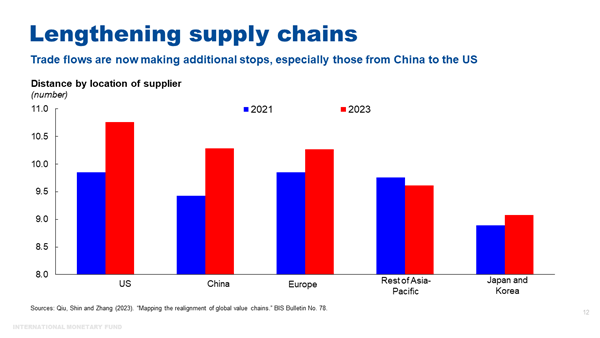

This anecdotal proof—together with correlations within the knowledge—level to lengthening provide chains. That is supported by a current BIS examine, which examined knowledge from greater than 25,000 corporations and located that offer chains have lengthened within the final two years, particularly these involving Chinese language suppliers, and US clients.

In sum, fragmentation is already a actuality as geopolitical alignments form commerce and funding flows: a course of that can probably proceed. However regardless of efforts by the 2 greatest economies to chop ties, it’s not but clear how efficient they are going to be in a deeply built-in and related international financial system.

The financial prices of fragmentation.

If fragmentation deepens, what could be the financial price? And the way will these prices be transmitted?

With commerce being the primary channel by way of which fragmentation may reshape the worldwide financial system, imposing restrictions on commerce would diminish the effectivity positive factors from specialization, restrict economies of scale on account of smaller markets, and cut back aggressive pressures.

The capability of commerce to incentivize within-industry reallocation and generate productiveness positive factors could be stifled. Much less commerce would additionally indicate much less data diffusion, a key good thing about integration, which may be lowered by fragmentation of cross-border direct funding.

Fragmentation of capital flows would restrict capital accumulation—due to decrease FDI—and have an effect on the allocation of capital, asset costs, and the worldwide fee system, posing macro-financial stability dangers and probably resulting in a extra risky financial system.

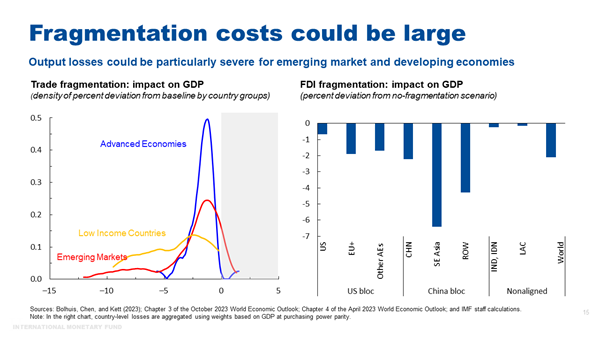

The estimates of the financial prices of fragmentation range extensively and are extremely unsure. However current and ongoing work on the IMF means that these prices could possibly be massive and weigh disproportionately on growing international locations.

If the worldwide financial system have been to fragment into two blocs primarily based on UN voting on the 2022 Ukraine Decision and commerce between the 2 blocs have been eradicated, international losses are estimated to be about 2.5 % of GDP. However relying on economies’ means to regulate, the losses may attain as excessive as 7 % of GDP. On the nation degree, losses are particularly massive for decrease revenue and rising market economies. [8]

FDI fragmentation in a world divided into two blocs centered across the US and China—with some international locations remaining non-aligned—may end in long run international losses of round 2 % of GDP.

As within the case of commerce, the losses are bigger for much less superior areas—which rely extra on inflows from the opposing bloc. [9]

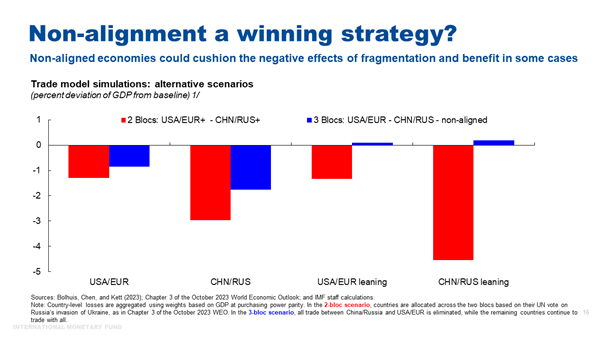

However lots will rely on how precisely commerce and funding fracture. If some economies stay non-aligned and proceed partaking with all companions, they might profit from the diversion of commerce and funding.

Our simulations recommend that if solely commerce between a US-Europe bloc and a China-Russia bloc is disrupted, the remaining economies will see some positive factors, on common. [10]

Latin American international locations are nicely positioned to learn in such a situation. For instance, Mexico’s proximity with america may increase its manufacturing sector, whereas South America’s commodity exporters may acquire market shares.

But when fragmentation worsens, even those that profit from fragmentation in its gentle varieties could possibly be left with a bigger slice of a smaller pie in an excessive situation. Briefly, everybody may lose.

Fragmentation would additionally inhibit our efforts to deal with different international challenges that demand worldwide cooperation. The breadth of these challenges—from local weather change to AI—is immense.

Latest IMF evaluation reveals that fragmentation of commerce in minerals crucial for the inexperienced transition—akin to copper, nickel, cobalt, and lithium—would make the vitality transition extra expensive. As a result of these minerals are geographically concentrated and never simply substituted, disrupting their commerce would result in sharp swings of their costs, suppressing funding in renewables and EV manufacturing. [11]

What can policymakers do to stop the worst-case financial situations in a full-blown Chilly Struggle II?

At this turning level, policymakers face troublesome tradeoffs between minimizing the prices of fragmentation and maximizing safety and resilience. Pragmatic approaches that protect the advantages of free commerce to the extent potential and safeguard fixing international challenges—whereas minimizing distortions—are wanted.

The primary finest answer, in fact, is to keep away from fragmentation. However, in the interim, this can be troublesome to attain.

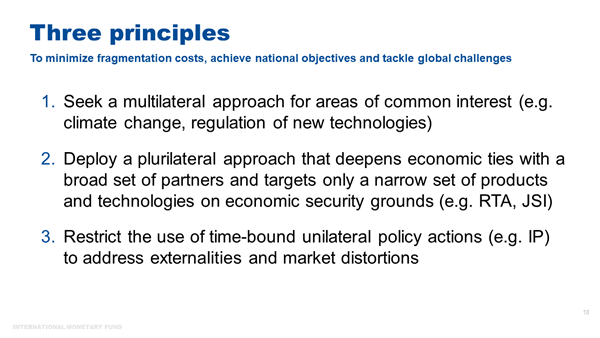

Absent the best-case situation, we should work to keep away from the worst-case situation and shield financial cooperation in a extra fragmented world. Three ideas might help:

First, search a multilateral strategy on the very least for areas of widespread curiosity. For instance, a inexperienced hall settlement may assure the worldwide move of minerals crucial for the clear vitality transition.

Comparable agreements for important meals commodities and medical provides may guarantee minimal cross-border flows in an more and more shock-prone world. Such agreements would safeguard the worldwide targets of averting local weather change devastation, meals insecurity and pandemic associated humanitarian catastrophe. [12]

Second, if some reconfiguration of commerce and FDI flows is deemed essential to de-risk and diversify, a non-discriminatory plurilateral strategy might help international locations deepen integration, diversify, and mitigate resilience dangers.

Policymakers ought to outline broadly the set of companions and allies with which to deepen financial partnerships. Plurilateral agreements in keeping with the WTO—akin to regional commerce agreements and joint assertion initiatives—whereas clearly second finest, may provide a number of advantages. These embrace economies of scale, higher market entry, and diversified suppliers, amongst others. By updating the foundations and protecting an open-door coverage, such agreements enable new companions to affix when they’re prepared and capable of decide to the agreements’ guidelines and norms.

Latest examples of regional commerce agreements (RTA) embrace the Complete and Progressive Settlement for Trans-Pacific Partnership (CPTPP) and the African Continental Free Commerce Space (AfCFTA). A number of joint assertion initiatives are at present underway, together with on e-commerce, funding facilitation, and companies home regulation. In December 2021, 70 WTO members agreed on a WTO-based plurilateral settlement on home regulation of companies.

Policymakers ought to goal solely a slender set of merchandise and applied sciences that warrant intervention on financial safety grounds. Earlier than deciding to deliver manufacturing dwelling, they have to fastidiously take into account whether or not there’s actually a scarcity of suppliers from much less dangerous areas and make an goal evaluation of the social and financial prices of provide disruptions. That is particularly the case for extensively used applied sciences, akin to semi-conductors.

Third, limit unilateral coverage actions—akin to industrial insurance policies—to addressing externalities and market distortions and be time-bound. Restrict their aim to correcting market failures whereas preserving market forces the place they will allocate assets most effectively.

It’s crucial to fastidiously consider industrial insurance policies, each when it comes to their effectiveness in attaining acknowledged outcomes and related financial prices, together with cross-border spillovers.

Domestically, industrial insurance policies could also be laborious to restrict or roll again given their concentrated advantages and subtle prices.

Internationally, such insurance policies could result in retaliation, which might deepen fragmentation. In line with current IMF estimates, if China introduces a subsidy, the probability that the EU imposes a commerce proscribing measure inside 12 months in response to the subsidy is 90 %.

An inter-governmental dialogue—or a session framework—on industrial insurance policies may assist enhance knowledge and data sharing and establish the affect of insurance policies, together with their unintended penalties throughout borders. Over time, regular strains of communication may assist develop worldwide guidelines and norms on the suitable use and design of business polices, making it simpler for corporations to regulate to the brand new setting.

On every of those three ideas, we are able to search for blueprints from the final Chilly Struggle. All through that interval, the US and Soviet Union made a number of agreements to keep away from nuclear disaster. Each superpowers subscribed to the doctrine of mutually assured destruction, figuring out that an assault by one would in the end result in whole annihilation.

If we descend into Chilly Struggle II, figuring out the prices, we could not see mutually assured financial destruction. However we may see an annihilation of the positive factors from open commerce. In the end, policymakers should not lose sight of these positive factors. It’s of their—and everybody’s—finest curiosity to advocate strongly for a multilateral rules-based buying and selling system and the establishments that help it.

In fact, financial integration has not benefited everybody—acknowledging that is crucial to understanding further motivations behind international inward shifts, and home insurance policies should regulate to broaden the advantages. However it has helped billions of individuals change into wealthier, more healthy, and higher educated—for the reason that finish of the Chilly Struggle, the dimensions of the worldwide financial system roughly tripled, and almost 1.5 billion individuals have been lifted out of utmost poverty.

Conclusion

Let me conclude. Whereas there are not any indicators of broad-based retreat from globalization, fault strains are rising as geoeconomic fragmentation is more and more a actuality. If fragmentation deepens, we may discover ourselves in a brand new Chilly Struggle.

The financial prices of Chilly Struggle II could possibly be massive. The world has change into rather more built-in, and we face an unprecedented breadth of widespread challenges {that a} fragmented world can’t deal with.

But, even on this new geopolitical actuality, policymakers can search options that reduce the prices of fragmentation. The main focus ought to be on pragmatic approaches that protect the advantages of free commerce to the extent potential, safeguard fixing international challenges, whereas attaining home targets of safety and resilience.

Maintaining open the strains of communication, as is being performed by the US, China, and EU, might help forestall the worst outcomes from occurring. The non-aligned international locations, that are primarily rising and growing international locations, can deploy their financial and diplomatic heft to maintain the world built-in. In spite of everything, many rising and growing international locations face the most important losses from a fragmented world, and whereas some profit within the early levels of fragmentation, all lose in a full-blown Chilly Struggle.

As we take into account this “turning level” query over the subsequent few days, I encourage all of us to consider how we might help obtain these options—by way of our analysis and our collaboration. This can be crucial to protect what we now have achieved and face the worldwide challenges forward.

Thanks.

References

Aiyar, Shekhar, Davide Malacrino, and Andrea Presbitero (2023a). “Investing in Associates: The Position of Geopolitical Alignment in FDI Flows.” CEPR Dialogue Paper 18434.

Aiyar, Shekhar, Andrea Presbitero, and Michele Ruta (2023b). “Geoeconomic Fragmentation: The Financial Dangers From a Fractured World Financial system.” CEPR Press.

Alfaro, Laura, and Davin Chor (2023). “World Provide Chains: The Looming “Nice Reallocation.” NBER Working Paper 31661, Nationwide Bureau of Financial Analysis.

Antràs, Pol (2021). “De-Globalisation? World Worth Chains within the Put up-COVID-19 Age,” (2021) ECB Discussion board: Central Banks in a Shifting World Convention Proceedings.

Attinasi, Maria Grazia, Lukas Boeckelmann, and Baptiste Meunier. 2023. “Pal-Shoring World Worth Chains: A Mannequin-Based mostly Evaluation.” European Central Financial institution Financial Bulletin 2, European Central Financial institution, Frankfurt.

Bolhuis, Marijn, Jiaqian Chen, and Benjamin Kett. 2023. “Fragmentation in World Commerce: Accounting for Commodities”. IMF Working Papers 23. Worldwide Financial Fund.

Bown, Chad (2022). 4 Years Into the Commerce Struggle, are the US and China Decoupling. Working paper, Peterson Institute for Worldwide Economics.

Caldara, Dario and Matteo Iacoviello (2022). Measuring Geopolitical Danger. American Financial Assessment 112 (4), 1194–1225.

Campos, Rodolfo, Julia Estefania-Flores, Davide Furceri, and Jacopo Timini (2023). Geopolitical fragmentation and Commerce.” Journal of Comparative Economics (Forthcoming).

Dang, Alicia, Kala Krishna and Yingyan Zhao. 2023. “Winners and Losers from the U.S.-China Commerce Struggle.” NBER Working Papers 31922, Nationwide Bureau of Financial Analysis.

Fajgelbaum, Pablo, Pinelopi Goldberg, Patrick Kennedy, Amit Khandelwal, and Daria Taglioni. 2023. “The US-China Commerce Struggle and World Reallocations.” American Financial Assessment: Insights (Forthcoming).

Ferguson, Niall. 2020. “Chilly Struggle II.” Nationwide Assessment Journal, December 3, 2020.

Freund, Caroline, Aaditya Mattoo, Alen Mulabdic, Michele Ruta. 2023. “Is US Commerce Coverage Reshaping World Provide Chains?” World Financial institution Coverage Analysis Working Paper 10593.

Góes, Carlos, and Eddy Bekkers. 2022. “The Impression of Geopolitical Conflicts on Commerce, Development, and Innovation.” Employees Working Paper ERSD-2022-09, World Commerce Group, Geneva.

Gokmen, Gunes (2017). “Conflict of Civilizations and the Impression of Cultural Variations on Commerce” Journal of Growth Economics, 127, 449-458.

Worldwide Financial Fund. 2023a. “Geoeconomic Fragmentation and International Direct Funding”. Chapter 4, World Financial Outlook, April.

Worldwide Financial Fund. 2023b. “Commodities and Fragmentation: Vulnerabilities and Dangers”. Chapter 3, World Financial Outlook, October.

Javorcik, B. Seata, Lucas, Kitzmueller, Helena Schweiger, and Muhammed Yıldırım (2022). “Financial Prices of Pal-shoring.” EBRD Working Paper 274, European Financial institution for Reconstruction and Growth.

Qiu Han, Hyun Tune Shin and Leanne Si Ying Zhang (2023). “Mapping the realignment of world worth chains.” BIS Bulletin No 73, October 3, 2023.

[1] Deglobalization refers back to the retrenchment of financial flows between international locations. Sometimes measured as a discount on the earth commerce (or funding) to GDP ratio, deglobalization could possibly be pushed by coverage decisions (such because the imposition of tariffs), secular tendencies (such because the structural transformation in direction of less-traded components of the financial system), and the waning of forces that helped spur the fast integration of economies till the mid-2000s (such because the discount in transport prices, the break-up of manufacturing processes throughout international locations, technological advances, and the like). Fragmentation, alternatively, refers to policy-induced redirection of commerce and funding flows which will or is probably not related to a decline in world commerce to GDP.

[2] See Antras (2021).

[3] In the course of the Chilly Struggle, the world was divided into two blocs, a Western and Japanese bloc, and a set of non-aligned international locations. The evaluation makes use of the bloc definition primarily based on Gokmen (2017). The Western bloc consists of Andorra, Australia, Belgium, Canada, Denmark, France, Germany, Greece, Iceland, Israel, Italy, Japan, Luxembourg, Malta, Monaco, Netherlands, New Zealand, Norway, Philippines, Portugal, San Marino, South Korea, Spain, Taiwan, Thailand, Turkey, United Kingdom, United States. The Japanese bloc consists of Albania, Armenia, Azerbaijan, Belarus, Bulgaria, China, Cuba, Czech Rep., Estonia, Georgia, Hungary, Kazakhstan, Kyrgyzstan, Lao Individuals’s Dem. Rep., Latvia, Lithuania, Moldova, Mongolia, North Korea, Poland, Romania, Russia (USSR), Slovakia, Turkmenistan, Ukraine, Uzbekistan, Vietnam. The remaining international locations are thought of “non-aligned.”

[4] For the present interval, the evaluation considers a hypothetical Western bloc, together with US, Europe, Canada, Australia and New Zealand. The hypothetical Japanese bloc contains Belarus, China, Mali, Nicaragua, Russia, and Syria. The remainder of the international locations are thought of “non-aligned.”

[5] See Aiyar et al. (2023a).

[6] See Fajgelbaum and Khandelwal (2022) for a survey of the literature, in addition to Alfaro and Chor (2023), Bown (2022), Freund et al. (2023),.

[7] See additionally Alfaro and Chor (2023), Dang et al. (2023) and Freund et al. (2023).

[8] See Bolhuis, Chen and Kett (2023). A rising literature additionally factors to massive prices from commerce fragmentation and the ensuing reshaping of GVCs (see, amongst others, Aiyar et al. 2023b; Attinasi et al. 2023; Campos et al. 2023; Goes and Bekkers 2023, Javorcik et al. 2022).

[9] See Chapter 4 of the April 2023 World Financial Outlook.

[10] Mixture international output modifications would nonetheless be destructive on this situation, because of the inefficiencies related to commerce restrictions even when utilized solely to a subset of the world economies.

[11] See Chapter 3 of the October 2023 World Financial Outlook.

[12] The worldwide group may be taught from the exemption of humanitarian meals purchases from export restrictions established on the twelfth WTO Ministerial Convention in 2022.