By Vance Ginn

Ranking company Moody’s simply downgraded China’s credit score outlook from steady to adverse after doing the identical to the US a few month in the past. Does this imply that China is on equal footing with us? Worse? Higher off?

An financial evaluation means that China shouldn’t be our largest risk, nor are we theirs. In truth, the most important drawback we face is totally self-inflicted and located on our dwelling soil.

Apprehensions about China’s army actions and commerce methods keep resonance, particularly amongst middle-aged and older Individuals. Whereas warning is warranted, particularly regarding their censorship and the therapy of Hong Kong and Taiwan, an financial comparability settles many doubts.

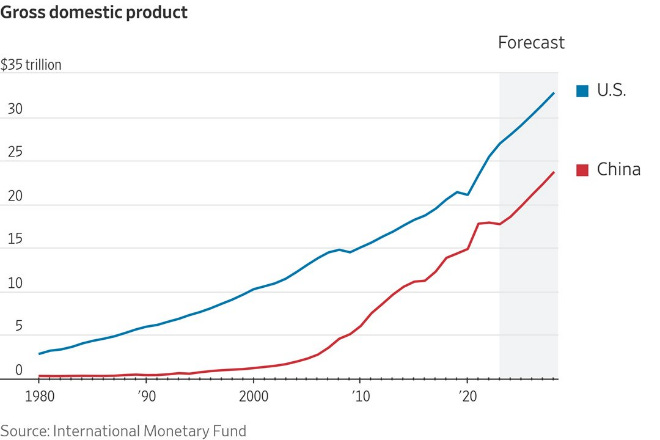

Concerning financial may, the US outshines China with a GDP of $27 trillion in comparison with China’s $18 trillion.

The distinction is stark on a per-capita foundation. Individuals get pleasure from a mean revenue of $79,000, six occasions greater than their Chinese language counterparts.

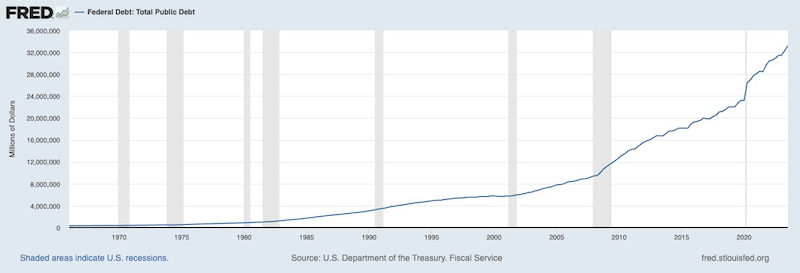

One alarming similarity stands out although: Each nations have weathered credit score downgrades primarily resulting from escalating price range deficits and nationwide money owed.

The US’ nationwide debt is shaping as much as be this decade’s hallmark. Now practically $34 trillion, the deficit spiked in 2020, with trillions of {dollars} extra added since. Internet curiosity funds on the debt climbed by 39 p.c and not too long ago surpassed $1 trillion yearly.

The repercussions of the nationwide debt disaster usually are not merely theoretical – they’re tangible, affecting the on a regular basis lives of residents.

In 2023, the greenback has considerably depreciated. Fitch (and now Moody’s) downgraded our creditworthiness. Residence gross sales hit their slowest tempo since 2010. Common 30-year mounted mortgage charges reached their highest level since 2000. And actual median family revenue dipped to its lowest stage since 2018, to call just some of our latest financial woes.

These findings shed new gentle on our competitors with China. They need to immediate America’s leaders to reevaluate our priorities and contemplate whether or not the enemy throughout the Pacific is as urgent as those we face at dwelling.

Whereas some argue the federal government spending that drove the deficits was obligatory, particularly through the pandemic’s peak, it underscores the broader drawback – a scarcity of fiscal self-discipline and a predisposition to depend on debt as a fast repair. It’s excessive time the US adopted a spending-limit rule. With out one, we’ve solely made issues worse and didn’t attain price range agreements.

An affordable spending restrict of not more than the speed of population growth plus inflationhas labored on the state stage, and it might work on the federal stage.

Whereas the US factors the finger at China, we now have three different fingers pointing again at us.

Extreme authorities spending and a burgeoning nationwide debt are eroding the inspiration of our financial stability. Now shouldn’t be the time to allocate extreme assets to confront exterior foes, however to handle the basic concern plaguing us: a authorities that refuses to rein in spending of taxpayer cash.

America must also right the errors in recent times of commerce protectionism.

There may be cause to counter these international locations who don’t play by the identical guidelines, like China, however that must be finished by becoming a member of free commerce agreements with allies. This is able to be a simpler and inexpensive method for Individuals as an alternative of elevating taxes on them by way of tariffs, appreciating the greenback thereby rising the commerce deficit and contributing to commerce wars that always result in army wars.

Let’s refocus our efforts, fortify our financial basis, and confront the real risk inside our borders. If not, governments won’t be able to do their job of preserving liberty. That is of utmost significance.

- Concerning the writer: Vance Ginn, Ph.D., is founder and president of Ginn Financial Consulting, LLC. He’s chief economist at Pelican Institute for Public Coverage and senior fellow at Younger Individuals for Liberty. He beforehand served because the affiliate director for financial coverage of the White Home’s Workplace of Administration and Finances, 2019-20. Observe him on Twitter @VanceGinn

- Supply: This text was printed by AIER